Types of Positive Pay: Standard, Payee, Reverse & ACH Explained

Comprehensive guide to the four types of Positive Pay systems: Standard, Payee, Reverse, and ACH Positive Pay. Learn how each protects against check and electro...

8 min read

Positive Pay is a fraud prevention service used by financial institutions to verify checks and protect businesses from unauthorized transactions.

Positive Pay is essentially an automated cash management service meticulously crafted to sniff out and prevent check fraud by verifying checks presented for payment against a compiled list of checks issued by a business. This verification sequence involves a cross-examination of essential check details like check number, monetary amount, and account number. Any incongruences are quickly flagged for further scrutiny, permitting the business to either sanction or decline the payment. By doing so, this system acts as a bulwark against financial losses and liabilities, granting businesses an extra shield of security in their financial dealings.

Positive Pay functions through an orchestrated series of systematic processes ensuring only authorized checks see successful processing. Here’s a step-by-step walkthrough:

This precise process ensures only legitimate checks pass through, acting as a defense line against fraudulent encroachments.

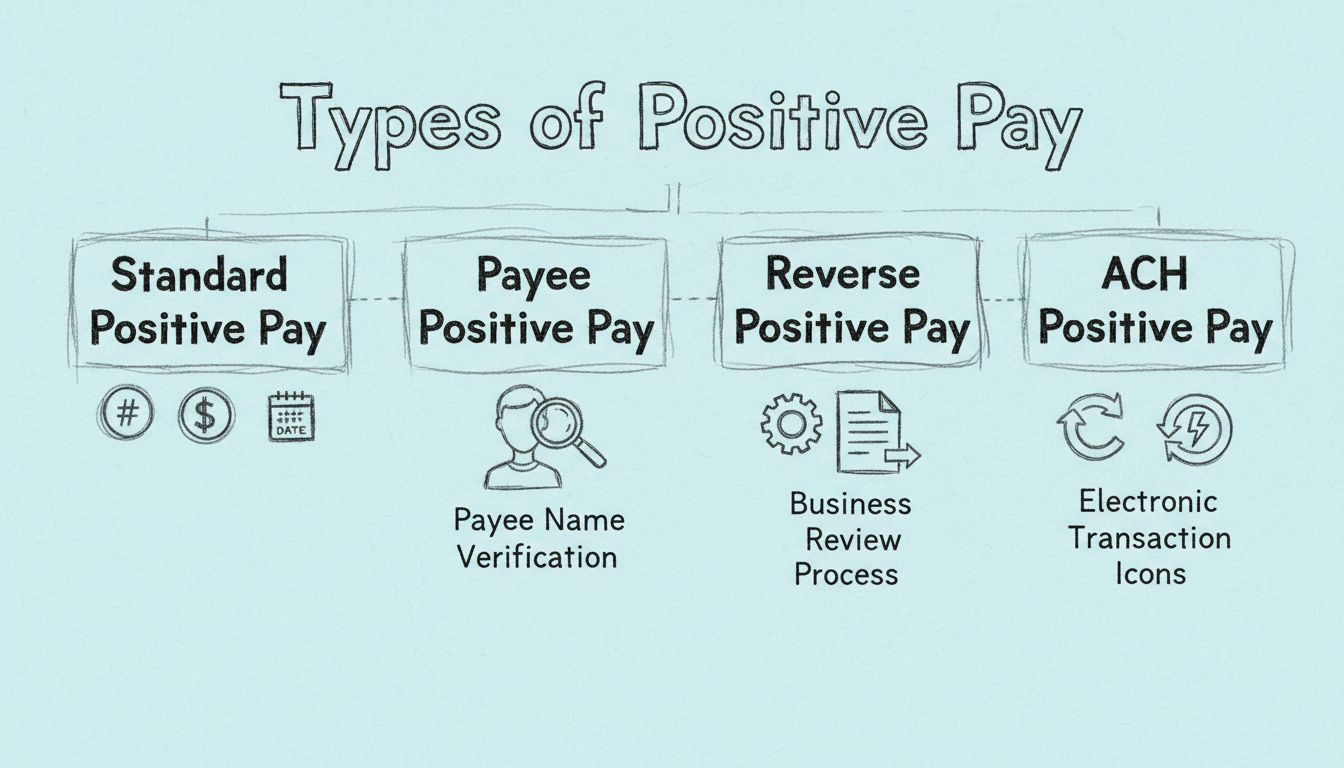

Positive Pay isn’t a monolith; it presents various forms tailored to meet specific fraud prevention exigencies:

The deployment of Positive Pay yields manifold advantages to businesses:

Bringing Positive Pay into play necessitates a concerted endeavor between businesses and their banking partners:

In affiliate marketing and accompanying software domains, Positive Pay has a notable role in preserving financial integrity. By securing financial transactions, businesses can guarantee that affiliate payouts and other financial interactions stay safe from fraud. Implementing Positive Pay can also enhance trust within affiliate networks, assuring affiliates of the security and legitimacy of their commissions and payments.

Set up advanced tracking in minutes. No credit card required.

With traditional Positive Pay, the bank takes the active role in fraud detection. The business submits a list of authorized checks, and the bank automatically compares each presented check against this list. The bank flags discrepancies and notifies the business, which then decides whether to authorize payment. This approach is often described as “set-it-and-forget-it” because once the initial setup is complete, the business primarily responds to exceptions rather than actively monitoring all transactions.

Reverse Positive Pay reverses this responsibility structure. Instead of the bank comparing checks against a business-provided list, the business receives a daily list of checks presented for payment and must actively review and approve each one. The bank then processes only the checks the business has approved. This method gives businesses maximum control over their transactions but demands significant daily effort. If the business fails to respond within the specified timeframe—typically 24 to 48 hours—the bank may automatically process the checks, potentially allowing fraudulent items through.

The choice between these approaches depends on several factors. Positive Pay suits businesses that prefer a more passive approach and trust their bank’s fraud detection capabilities. Reverse Positive Pay appeals to businesses that want maximum control and have the resources to dedicate staff to daily check review. Most financial experts recommend traditional Positive Pay for most businesses due to its balance of security and operational efficiency.

False positives occur when legitimate checks are flagged as exceptions due to minor discrepancies—data entry errors, check number sequencing issues, or timing mismatches between when checks are issued and when the Positive Pay file is submitted. Implementing quality control procedures for file creation minimizes these.

Missed deadlines represent a significant risk, particularly with Reverse Positive Pay. Establishing clear procedures with designated staff responsible for timely exception responses helps prevent this. Many banks offer automated decision rules for certain exception types.

File submission errors (incomplete or inaccurate Positive Pay files) can result in legitimate checks being rejected or fraudulent checks being processed. Reconciling the Positive Pay file against the check register before submission catches errors early.

Integration challenges may arise when connecting Positive Pay systems with existing accounting software. Working with both the bank and accounting software vendor ensures smooth integration; most modern accounting systems include built-in Positive Pay file generation.

Be the first to know about new features and product updates.

Maintain accurate and timely file submissions — all check information must be correct and submitted promptly, ideally daily, to ensure the bank has current data when checks are presented.

Establish clear internal controls — segregate duties so the person authorizing checks differs from the person creating the Positive Pay file. Regular audits of the process identify errors before they impact operations.

Promptly review and act on exceptions — delays in responding can result in checks being automatically processed or rejected. Establish a clear review and decision-making process with designated staff.

Select comprehensive service features — for most businesses, Payee Positive Pay represents the minimum recommended protection. Businesses with significant ACH volumes should also consider ACH Positive Pay.

Monitor and adjust rules regularly — for ACH Positive Pay or Reverse Positive Pay, review and update rules quarterly to reflect changing vendors, transaction limits, and business needs.

Enhanced authentication methods are expanding beyond basic data matching—including image-based verification where digital images of checks are compared against submitted data, and biometric authentication for check authorization.

Artificial intelligence and machine learning are being integrated to improve fraud detection accuracy. AI algorithms identify patterns in exception data that indicate emerging fraud schemes, while machine learning models reduce false positives by learning from historical data.

Integration with digital payment systems is extending Positive Pay’s reach beyond paper checks to ACH transactions, wire transfers, and other electronic payment types.

Real-time processing is becoming the standard as banks invest in faster infrastructure, allowing checks to be cleared or rejected immediately upon presentation rather than waiting for batch processing.

Unlock the language of affiliate marketing and master key terms to succeed in your efforts.

Comprehensive guide to the four types of Positive Pay systems: Standard, Payee, Reverse, and ACH Positive Pay. Learn how each protects against check and electro...

Explore the Positive Shift affiliate program, offering online personal training and exercise rehabilitation by experienced kinesiologists. Learn about its CPS-b...

Join our community of happy clients and provide excellent customer support with Post Affiliate Pro.

Cookie Consent

We use cookies to enhance your browsing experience and analyze our traffic. See our privacy policy.